Lithium-ion battery recycling still not that close

Lithium-ion (Li-ion) battery recycling is not expected to take off before 2030, according to a new report by Wood Mackenzie. Last year, EVs accounted for just under 7% of passenger car sales globally, and Wood Mackenzie’s base case scenario expects penetration to reach 23% by 2030. The transition to the massive scale-up of EVs naturally points to an equally high demand for Li-ion batteries. By 2040, 89% of Li-ion battery demand will come from the EV sector.

Wood Mackenzie research analyst Max Reid said: “Underneath the surface of this electric future lies a relatively young supply chain struggling to keep up. The Li-ion battery demand market can fluctuate over months and expanding upstream and midstream to produce battery materials involves lead times of several years. As it is a new industry, there is limited historic capacity to flip the switch on, and yet many see this as a ripe environment for recycling to make a tangible impact.”

Reminder that flooded lead-acid batteries are nearly 100 percent recyclable.

Why? Currently, battery recycling focusses on the portable electronics market. Recyclers benefit from technologies with an easily accessible battery, compared with EV batteries. EV-packs are complex to disassemble into individual cells, so recyclers are left to discharge packs in conductive baths before mechanically shredding them into a mix of constituent materials. Furthermore, currently new batteries cost less to produce, hence disincentivizing battery recycling as the value of recovered material is reduced.

Also, battery manufacturers are leaning toward using cheaper materials, leaving recyclers to increase the efficiency of their processes to maintain profit. Moreover, the introduction of new materials such as solid-state electrolytes will require recyclers to retrofit their processes.

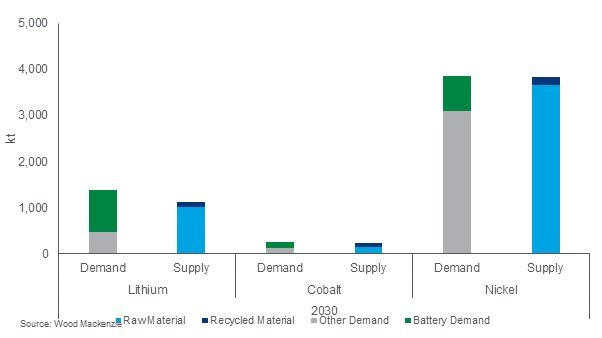

Secondary supply will not make up for a supply imbalance for the three critical battery materials

Reid said: “This decade will see the supply chain further establish itself to be able to supply vast quantities of battery-grade chemicals and cathodes to cell manufacturers, whilst recyclers will struggle with the large mass and complexity of EV-packs.”

A new cathode facility will produce 50 kilo-tonnes per annum (ktpa) of NMC (nickel, manganese and cobalt) material, whilst a recycling facility will typically process 5-10 ktpa of e-waste – the former equating to roughly 400,000 battery EVs annually and the latter taking in just roughly 30,000 EV-packs yearly.

Reid also pointed to the lack of recyclable feedstock as a major barrier. Even though EV manufacturing is set to boom before 2030, the number of end-of-life (EoL) batteries available for recycling will remain limited for two main reasons: EV penetration at the beginning of the decade is much lower than at the end, and EVs have an increasingly long lifespan reaching up to 15 years.

The lack of available secondary supply from recycling is evident, and yet the recycling sector is already scaling up quite aggressively. According to Wood Mackenzie’s analysis, the total capacity of planned recycling facilities will still overshoot feedstock in 2030 when EoL EV numbers begin to ramp up.

The resulting supply imbalance will leave independent recyclers, especially in North America and Europe, in a scramble for used EV batteries. China, which has a mature and large re-use and refurbishment sector for portable electronics, benefits from proximity to the midstream. Chinese recyclers benefit from greater integration with nearby cathode production plants, so Chinese recyclers can regularly bid much higher prices for used batteries than their Western counterparts. Until North America and Europe have developed more integrated raw material supply chains, China will remain the most appealing location for battery recycling.

Reid said: “Bullish expectations for Li-ion recycling may well lead to a rush of new entrants to the space. However, limitations on feedstocks mean that only the large and integrated will likely survive and reap the rewards in later years.”

Comments are closed here.