GTM Research predicts solar market doomsday scenario if Suniva’s proposal is approved

If SEIA’s 88,000 job loss warning wasn’t enough, GTM Research has published a chilling report on the devastating impact Suniva’s new trade dispute would have on the U.S. solar market if their proposals were imposed.

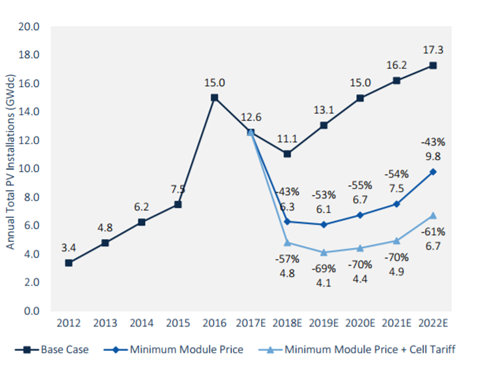

If Suniva’s petition is successful, GTM says it will erase two-thirds of what’s expected to come online over the next five years with utility-scale solar being the most at risk. If module prices returned to 2012, immediately with more than 20 GW would be at risk of being canceled. If Suniva’s proposal is approved — meaning, there will be a new minimum price on imported crystalline silicon solar modules, and a new tariff on imported cells — the U.S. could miss out on more than 47 GW of solar installations. That’s more than what the U.S. solar market has brought online to date.

“In our latest report we found that between 2018 and 2022, total U.S. solar installations would fall from 72.5 GW cumulatively to just 36.4 gigawatts under a $0.78 per watt minimum module price scenario. Even more dramatic, with a $1.18 per watt minimum price, representing a $0.40 per watt cell tariff on top of a $0.78 per watt minimum module price, cumulative installations would plummet to 25 gigawatts.”

SEIA explains plan to lead fight against Suniva petition, remedies for the future

Key Findings: Section 201 Scenario Analyses

• Between 2018 and 2022, total U.S. solar installations would fall from 72.5 GW cumulatively to just 36.4 GW under a $0.78/W minimum module price scenario, or 25 GW under a $1.18/W minimum price, representing a $0.40/W cell tariff on top of a $0.78/W minimum module price.

• Utility PV is expected to see the largest downward revisions to its base case forecast. A majority of utility PV procurement now hinges on solar being cost competitive with natural gas alternatives, with nearly three-fourths of the utility PV pipeline procured outside Renewable Portfolio Standards. Under both tariff scenarios, most of that is at risk of cancellation unless PPA prices are renegotiated.

• Residential PV is the least sensitive segment to the introduction of tariffs. On one hand, the number of state markets at grid parity in 2021 would fall from 43 to 35 in the minimum module price only scenario (43 to 26 with the cell tariff added to the minimum module price). However, the top six states, which drive a majority of the base case outlook, would continue to offer more than 10% annual net savings. Challenging rate structures that limit savings for large C&I, plus financing risks for community solar, are the primary drivers behind non-residential PV experiencing a larger downturn than residential PV.

• Top tier module suppliers are sold out through the end of the year, as developers and installers contract imported modules ahead of a potential November ruling. Two-thirds of this supply will go to utility PV buyers who have better pipeline visibility, larger volumes and tighter project economics

Comments are closed here.