U.S. installed 8.4 GWh of BESS in Q1, surpassing previous record by 54%

The U.S. energy storage market hit new heights in Q1 2026, with a 54% increase over the previous Q1 record, according to a new report.

The United States installed a record 3.3 GW / 8.4 GWh of battery energy storage systems (BESS) in Q1 2026, as utility, commercial and residential installations all reached new highs, according to the latest U.S. Energy Storage Monitor report released today by the American Clean Power Association (ACP) and Wood Mackenzie.

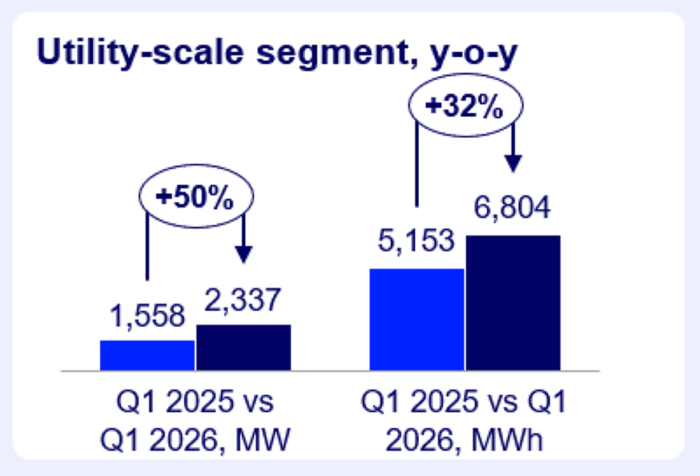

Utility-scale activity dominated the market, with more than 2.3 GW / 6.8 GWh installed in Q1 2026. The growth was largely driven by 2025 project delays as developers focused on meeting tax incentive eligibility deadlines for pipeline projects in the second half of 2025. Texas, California and Arizona continued to top the charts, but new markets with vertically integrated utilities also gained traction, particularly in Michigan and Georgia.

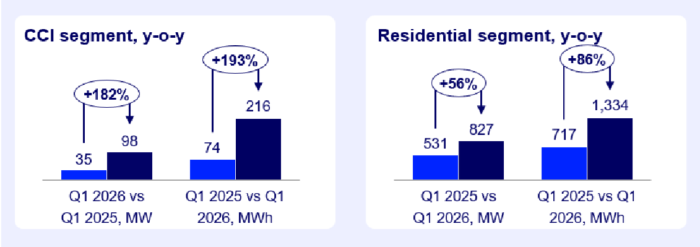

The Community, Commercial and Industrial (CCI) sector installed 97.7 MW in Q1 2026, an increase of 27% compared to Q4 2025, driven by California’s 75 MW installed. The report forecasts continued growth in the Illinois, Maryland, Massachusetts and New York community storage markets, with more than 215 MW in the collective project pipeline.

The U.S. residential segment installed a record 1.3 GWh in Q1 2026, up 86% year-over-year and 5% quarter-over-quarter, with volumes buoyed by an overflow of installations initiated at the end of 2025 to capture the expiring Section 25D tax credit. California, Texas, Hawaii and Arizona had the largest increases compared to Q4 2025 in storage capacity deployed in the first quarter of this year.

“The industry is delivering on what the market needs, fast, flexible power that supports load growth, resource adequacy, and a modern grid,” says John Hensley, SVP of market and policy analysis at ACP. “These record-breaking battery storage installations underscore the critical role storage plays in maintaining grid reliability and the strong value that utilities, corporate purchasers, and grid operators see in the technology.”

U.S. storage market expected to nearly quadruple over next 6 years

BESS installations are projected to reach 200 GW / 655 GWh of cumulative installed capacity by 2031, according to the U.S. Energy Storage Monitor report, driven mainly by the utility sector, which will make up 85% of installations between 2026 and 2031.

“Co-location and contracting with large loads will be a key market driver for the foreseeable future,” says Allison Feeney, research analyst at Wood Mackenzie. “Utility-scale is poised for the most explosive expansion, but the CCI market will grow a steady 26% by 2031 as well. Despite a strong start to the year, we do see residential contraction 5% in 2026, due to constraints in tax equity availability, and updated permitting rules.”

Trade restrictions could cause bottlenecks

With foreign entity of concern (FEOC) restrictions now in force, the challenge of securing FEOC-compliant equipment and safe harbored capacity will be a critical developmental bottleneck over the next 2-4 years.

“Developers with mature pipelines and available capital rushed to safe harbor their pipelines in late 2025 and will now work to secure long-term supply agreements with domestic manufacturers for the rest of their pipeline,” says Allison Weis, global head of storage at Wood Mackenzie. “Lower tier developers either face acquisition or turn to low-cost Chinese OEMs. Battery energy storage cell manufacturers will work to secure limited FEOC-compliant cell components to qualify for the 45X tax credit, a key factor in maintaining cost competitiveness with China.”

Sensible trade policies that support rather than undermine supply chains can enable domestic supply chain development. ACP’s annual State of Clean Energy Manufacturing report found that most of the critical battery storage supply chain could be domestically supplied by the end of the decade, based on facilities currently under construction and announced investments.

Notable Market Developments:

- The CCI sector grew 193% year-over-year in Q1 2026, the strongest Q1 on record for the sector. California alone accounted for 75 MW of the 97.7 MW installed.

- The national residential solar-plus-storage attachment rate reached 45% in Q1 2026, up from 38% in Q1 2025, reflecting growing consumer demand for paired solar and storage installations.

- The U.S. is projected to install 146 GW / 499 GWh of new storage capacity between 2026 and 2031, underscoring the scale of the build-out ahead as the grid modernizes to meet rising load.