U.S. Community solar market declines 36% in 2025

The first half of 2025 has seen a sharp dropoff in community solar installations in the United States, according to a new report by Wood Mackenzie in collaboration with the Coalition for Community Solar Access (CCSA). After a record-breaking year in 2024, the U.S. community solar market decline 36% in the first half of 2025 in a year-over-year analysis, resulting in 437 MWdc of new capacity installed.

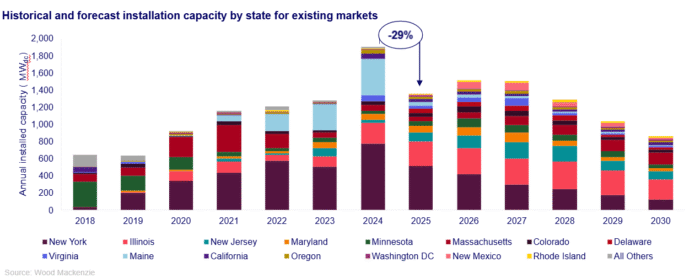

Because of the passage of the One Big Beautiful Bill Act (OBBBA) and related federal policy changes, Wood Mackenzie’s cumulative five-year community solar outlook decreased by 8% compared to the outlook published in Q2 2025. The passage of the OBBBA has fundamentally altered the long-term market landscape, while slowing growth in mature markets, particularly New York’s community solar program, is contributing to an expected 29% national contraction in 2025.

“Overall, we expect national installed community solar capacity will contract by an average of 12% annually through 2030,” said Caitlin Connelly, senior analyst and lead author of the report. “The final bill offers a crucial four-year window for projects already under development to come online and secure the Investment Tax Credit (ITC), supporting near-term buildout. As of mid-2025, there are over 9 GWdc of community solar projects under development, with over 1.4 GWdc known to be under construction.”

Growth in emerging markets slows

According to the report, the market contraction in H1 2025 is primarily driven by steep declines in volumes in New York and in Maine, where the current program was recently overhauled. Programs in some major state markets are close to or at capacity, and several programs in states including Maryland, Massachusetts, and New Jersey remain stalled in transitions between program iterations.

New state markets could bring more capacity to the market, but there has been limited success in passing community solar program legislation so far this year.

“The early expiration of the ITC will only add to this difficulty given the window for any new projects to secure tax credits is so small,” Connelly said . “The passage of legislation in new markets could potentially add upwards of 1.1 GWdc through 2030.”

CCSA president and CEO Jeff Cramer urges highlighted some bright spots in the market, but urged action to take advantage of the opportunity.

“Customer demand for community solar has never been stronger, and we’re seeing states step up with historic expansions like New Jersey’s 3,000 MW and Massachusetts’ 900 MW,” Cramer said. “These bright spots show what’s possible when policymakers work to unlock capacity. At the same time, this report makes clear the challenges ahead, from federal uncertainty to interconnection delays and program caps, that must be addressed to realize the full potential of community solar and deliver the resilient, affordable power communities are asking for.”

Subscriber acquisition costs down, challenges for LMI market

Subscriber acquisition costs contracted 5% from H2 2024 on average across all customer segments. Corporate demand for community solar remains high, driving up commercial solar’s share of total community solar capacity to 53%. However, developers and subscription management companies face increased headwinds in subscribing low-to-moderate income (LMI) customers. Difficult subscriber acquisition dynamics lowered the share of community solar capacity serving low-to-moderate income (LMI) subscribers to 9%. The customer segment remains the costliest to subscribe at $102/kW compared to $72/kW for non-LMI residential customers.

Developers seek new growth opportunities

As new community solar programs struggle to take off, community solar developers increasingly target alternative distributed solar programs as pathways for long-term growth.

“Non-residential distributed solar, which typically encompasses projects sized between 2 to 20 MWdc, is extremely well-positioned for growth,” Connelly said. “Utilities are increasingly appreciating the value of community-scale resources because they can be deployed quickly, with storage, and close to customer load.”

Market Outlook and Scenarios

Cumulative community solar installations currently total 9.1 GWdc and are projected to exceed 16 GWdc by 2030. Wood Mackenzie has developed high-case and low-case scenarios to capture market uncertainties:

- High case: An 18% uplift to the five-year outlook through favorable state policy changes and efficient interconnection reform, adding 1.3 GWdc.

- Low case: A 16% contraction due to complex tax credit qualification guidelines and limited state intervention, reducing outlook by 1.2 GWdc.

Comments are closed here.