Price of polysilicon expected to steeply fall in 2023. Are module prices next?

The price of polysilicon is to fall steeply from the start of 2023, according to new Rethink Energy research tracking production capacity expansion plans announced by nineteen Chinese companies. With millions of tons planned, up from today’s global capacity of 880,000 tons, with investment costs running to the tens of billions of dollars, the most likely outcome is another decade of overcapacity and prices bumping along at marginal production costs.

Even if no new factories begin construction from this point on in August 2022, those already in the works, with investment committed, are enough to more than quadruple global output and render the past two years of high polysilicon prices nothing more than a bad dream.

“The claim made recently by LONGi – the world’s biggest wafer maker – that 1,000 GW could be manufactured each year by 2030, is not far from Rethink’s predictions. Before long manufacturing solar panels will be overtaken by grid integration as the most pressing constraint on the energy transition.

“Data coming out of organizations like China Minmetals Corporation and the China Photovoltaic Association shows capacity utilization of existing factories right now is almost 100% and new factories are being successfully ramped up in record time”, notes Andries Wantenaar, solar analyst and research lead for this paper.

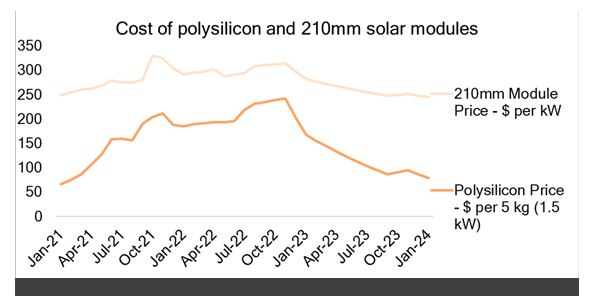

Impact on solar module prices

Solar supply chain price data collated from the past two years demonstrate that the price increases of solar modules, set to continue for the rest of this year, have been almost exclusively guided by the polysilicon price, itself little influenced by changes to cost of production, and mostly guided by opportunism in a seller’s market.

Module price impacts from non-polysilicon elements such as glass, backsheets, silver paste and more have all been of far lower magnitude throughout the whole pandemic-lockdown-reopening period.

Companies announcing polysilicon factory plans range from all of the existing Chinese players to downstream solar manufacturers looking to secure in-house supply, to actors in electronics-grade and industrial-grade silicon.

What about the U.S.?

As for the remaining Western polysilicon production capacity, some of which is brought back online having been shuttered during the 2018 to 2020 price slump, its ability to weather the coming storm will be dependent on a combination of tariffs, sanctions, and manufacturing incentives, such as those included in the Biden Administration’s Inflation Reduction Act – and it really will take a combination of all three to sustain a fully verticalized silicon-based photovoltaic supply chain anywhere outside of China.

The same can be said for India, where module and cell manufacture is being at least partially re-shored, but necessary policies to reclaim the wafer and polysilicon supply chain segments have yet to be brought into force.

Indonesia’s plans for a 200,000-ton polysilicon production capacity, if they are followed through on, will require similar. On the upside, both countries could become exporters to Western wafer factories, in a scenario in which China’s solar panels are fully excluded from the US, EU or other countries.

Comments are closed here.