New polysilicon capacity, TOPcon replacing PERC and more PV supply insights via CEA

New polysilicon capacity will soon start to normalize (lower) solar PV prices, and module manufacturing lines will start replacing PERC with TOPcon and heterojunction (HJT), according to interviews conducted by the Clean Energy Associates (CEA) Market Intelligence team for its Q4 2021 PV Supplier Market Intelligence Program Report (SMIP).

The subscription-only report, authored by CEA’s Market Intelligence team, includes proprietary insights gathered from 1-on-1 interviews with technical leaders at many of the world’s leading solar suppliers. CEA’s Q4 2021 SMIP report analyzes the progress of capacity expansions catering to large wafer modules and other power-boosting module technologies.

Here are some highlights:

Over 500,000 tonnes of new polysilicon capacity is coming online. Prices are expected to lower accordingly.

With the rapid removal of most energy control restrictions in China in Q4 2021, many polysilicon makers are now rushing to ramp up new capacities to take advantage of high polysilicon prices while supplies remain constricted.

The first tranche of polysilicon expansions, which started in late 2020, are starting to come online. Many will finish ramping up to full production in early to mid-2022, releasing a significant amount of new polysilicon into the market. Despite many follow-up expansions still in construction, both new and established suppliers are continuing to announce new polysilicon production capacities.

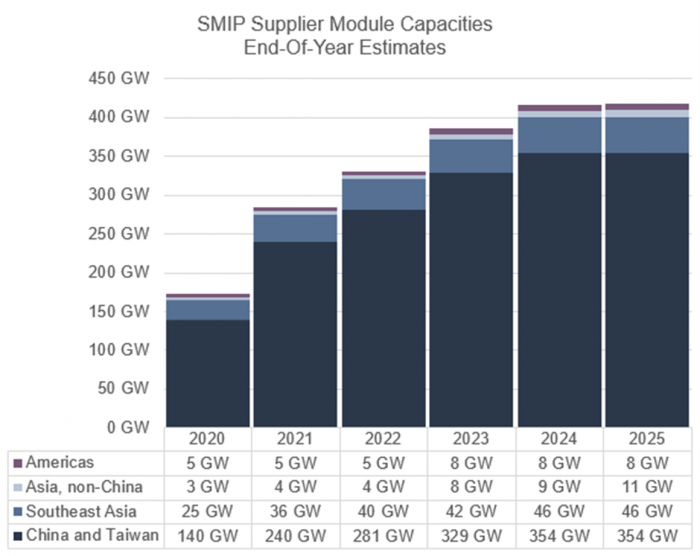

Production line updates led to slowdown in module capacity expansions

Fourth-quarter module and cell capacity expansions were smaller than expected, as many suppliers took old equipment offline and GCL exited cell production entirely. Some expansions did not materialize by the end of 2021 due to a challenging global manufacturing environment and trade tensions with the United States.

With a more robust outlook projected, ingot, wafer, cell, and module capacities will continue to increase over the next two years, with around 45 GW of additional module capacity slated to come online by the end of 2022 followed by over 55 GW of new module capacity in 2023.

TOPCon and HJT cell capacity is on the upswing

In addition to many suppliers reaching PERC cell efficiencies of 23.0% or higher, several established players and new entrants have announced TOPCon and HJT cell capacities. While many new entrants are suspected of not bringing these production lines online at the scale or timeline previously announced, many interviewed suppliers have made progress in implementing these upgrades.

Most suppliers are expected to convert existing PERC lines to TOPCon within the next few years to break past PERC’s commercial efficiency threshold of about 23.7%.

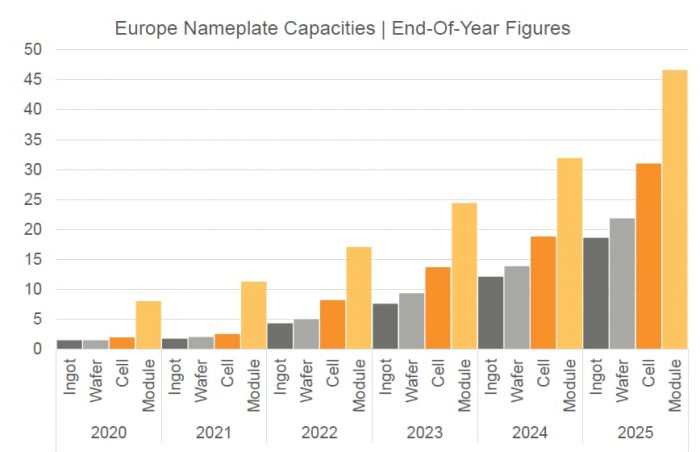

European suppliers have big plans, but the biggest are only in planning right now

Europe has a strategic interest in rehoming PV manufacturing capacity from ingot to module production due to high logistics costs, volatile energy commodity prices, and political interest in decoupling supply chains from China. Ingot, wafer, and cell production capacities will see the largest relative increase over the next few years, with ingot and wafer capacities potentially growing tenfold to over 20 GW by the end of 2025. Cell capacities currently total approximately 2.5 GW, and these capacities could grow to over 30 GW over the next four years based on current supplier expansion plans.

China’s 2022 Dual Control Policy clarified

In 2021, the Chinese government announced “Dual Control” policies on energy consumption and energy intensity. Energy generation control measures in Q3 and early Q4 2021 led to intermittent energy shortages and price increase of all main PV module inputs. China’s central party is planning to make Dual Control policies less disruptive in 2022 by making the policy’s objectives clearer. Consumption of energy from new renewable generation capacities may not face generation restrictions and will not be counted in provincial energy targets.

Comments are closed here.